Most counties in the state of Colorado sell tax liens in the months of October and November. Since tax liens are a stereotypical “Thing Rich People Do,” I was interested in investing in them. However, figuring out the expected return on them was a task.

In Colorado, tax liens are at a 10% interest rate. The interest is accumulated monthly and not compounded; however, the lien can be subtaxed each year, meaning that the holder can opt to pay the county the prior year’s taxes in exchange for rolling the amount, and also the prior year’s interest, into the lien. The lien may be redeemed at any time, meaning it is quite possible for redemption to happen the day after the lien is purchased. In that scenario, the minimum interest that can be accumulated is one month’s interest.

Most lien auctions in Colorado are on a premium basis — meaning that you bid a fixed amount over the face value. The premiums are usually put in the context of the percentage over the face value. For example, say that I purchase a lien for $100 at 5% premium. This means I paid $105 for the lien, $5 above the face value. The lien will accumulate only 83 cents in interest each month, so I will need to hold the lien for at least 6 months to break even. If the buyer redeems the lien before 6 months, I have lost money.

Therefore, in estimating profits from tax liens, the very first step was to estimate the rate of redemption. Information about this is surprisingly scarce on the web. Thankfully, El Paso County publishes redemption statistics.

The statistics are not archived, thus the numbers here may not match up with what is currently on the official website. At the time of September 2014, numbers I got were as follows:

- For tax liens in 2010: 6.7% were still unredeemed at the start of 2014 and 4.87% were still unredeemed in September 2014.

- For tax liens in 2011: 18.47% were still unredeemed at the start of 2014 and 9.9% were still unredeemed in September 2014.

- For tax liens in 2012: 27.1% were still unredeemed at the start of 2014 and 16.23% were still unredeemed in September 2014.

- For tax liens in 2013: 66.10% were still unredeemed at the start of 2014 and 35.5% were still unredeemed in September 2014.

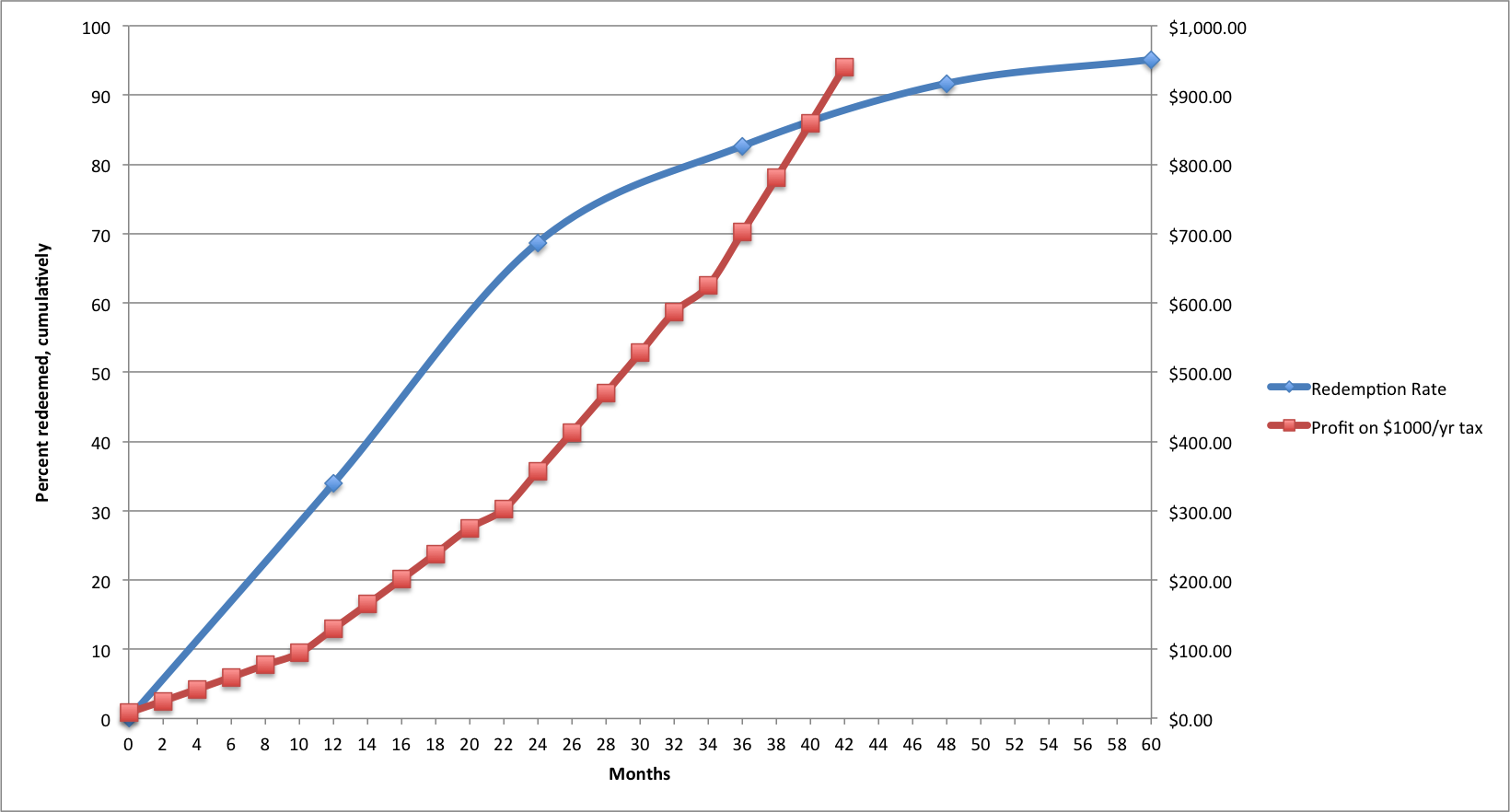

Now, for obvious reasons, it is dangerous to assume that liens issued in El Paso in certain years are representative of Colorado liens or predictive of any future liens. But it’s the best I had to go on. I plotted a graph in Excel:

Tax lien statistics. Red reflects profit on a $1000 investment. Blue reflects the redemption percentage.

So, we can expect 1/3 of liens to be redeemed in the first year, 2/3 in the second year, and 85% by the third year. The 40-month mark is an important milestone, because it is at that point where the lienholder can file to get the property altogether; for that reason, I did not calculate profits beyond that month. The profits assume the holder will subtax the liens, hence the slight jumps at these marks.

In future blog posts, I will explain the Monte Carlo simulator I created with this data, my findings, and my actual experience & returns-to-date.