The lien auction was online, and register bidders could compete with each other, just like eBay. Being a seasoned eBay veteran and former consigner’s assistant, I knew to wait until the last day of the auction to start sniping.

Intermission: What are tax liens?

The feedback I’ve gotten so far has been: “uh, what are tax liens?” Here, I backtrack to explain what tax liens are.

Tax Liens Part III: Deciding how much to bid

In Part II, I narrowed down a list of thousands of liens to roughly 30 I wanted to bid on. Now came the hard part: how much should I bid for these liens?

I built a Monte Carlo simulator that took in several parameters:

- Number of liens

- Average lien price

- Average premium percentage

- Number of iterations to simulate

Looking at the chart from Part I, there is a roughly 15% percent chance that the lien is never redeemed by the property owner. Yet, Colorado claims transfer of deed happens in less than one percent of all purchases. How can that be? I believe this is because most elect to not to go through the transfer of deed, because the lien they end up with is a dead end property as described in Part II. Since I narrowly targeted properties, this was not a concern for me. I thus marked liens that went past 40+ months as a “transfer of deed” with a conservative $15,000 return.

Still, this didn’t sit well with me even though El Paso’s statistics clearly indicated a nontrivial number of liens remained unredeemed past 40+ months. So, in the simulator, I separated the “non-house” iterations from those that “won” a house to give me a better view of what would happen if all of my liens would be redeemed.

So my output looked like this for 7 liens, $1200 each, 8% premium, 10000 iterations:

Over 10000 iterations:

Average outlay: $18693.12

Subtaxed the next year: 3.96 Pct: 0.57%

Average profit: $17459.30; 93.40%

Number of losing iterations: 36; 0.36%

Number of iterations without houses: 3822; 38.22%

Average outlay (no house only): $17640.92

Average profit (no house only): $1331.01; 7.55%

Number of losing iterations (no house only): 36; 0.94%

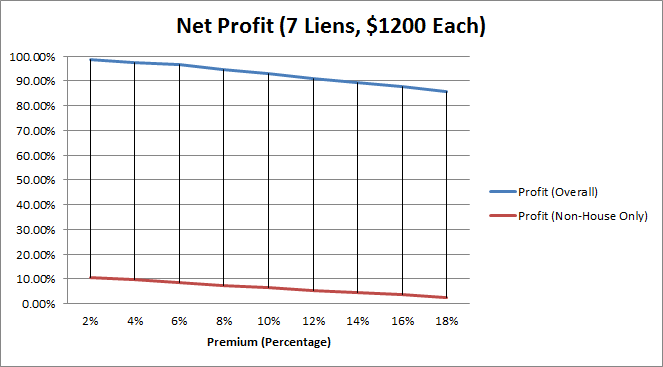

Here’s an Excel graph of estimated profits over increasing premiums using the same inputs, divided between house and non-house:

The net profit I would make on tax liens, with and without the assumption I’d get a transfer of deed.

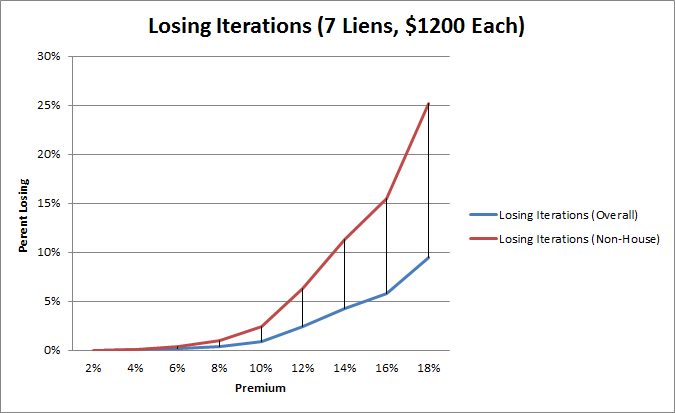

Another view, the percentage of time I would lose out:

Percentage of the time I would lose money on a tax lien.

Obviously, the premium played a big factor into the “riskiness” of the tax liens and the net profit I’d make on them. We agreed to bid up to 10% on them, as that still had a low chance that we’d lose out plus they would yield a generous 6.57% on average even if we wound up with no transfer of deed.

Now it was time to bid! Part IV covers what happened at the auction and thereafter. You may download my crappy Perl code if you wish, here: tax_lien_monte_cristo

Tax Liens Part II: Picking out the targets

Part I describes how I derived an estimated rate of redemption from my liens. Next came determining which liens to buy; there were thousands to choose from. Time to start building a script.

The goal, obviously, is to maximize returns on liens. There are two ways to lose out on liens:

- Property owner redeems the lien too early. This scenario was covered in Part I — the interest rate accrues at 0.83% monthly, and so in order to make a profit, the lien must be held for as many months as it takes to overtake the premium.

- Property owner never redeems the lien on an unprofitable property. In Colorado, when a property is passed to a lienholder, it comes free of most debts including mortgage debts, so responsibility for old debts is usually not a worry. Rather, the worry is that the lienholder could end up with a property that is unable to be turned over for a profit — for instance, a house that is actually a hollowed-out meth factory or more commonly, a parcel of desert land no one would ever buy.

Looking through the list of available properties showed a surprise: many property owners were corporations, businessmen, or real estate speculators.

Tax Liens Part I: Estimating redemption rates

Most counties in the state of Colorado sell tax liens in the months of October and November. Since tax liens are a stereotypical “Thing Rich People Do,” I was interested in investing in them. However, figuring out the expected return on them was a task.

In Colorado, tax liens are at a 10% interest rate. The interest is accumulated monthly and not compounded; however, the lien can be subtaxed each year, meaning that the holder can opt to pay the county the prior year’s taxes in exchange for rolling the amount, and also the prior year’s interest, into the lien. The lien may be redeemed at any time, meaning it is quite possible for redemption to happen the day after the lien is purchased. In that scenario, the minimum interest that can be accumulated is one month’s interest.

Most lien auctions in Colorado are on a premium basis — meaning that you bid a fixed amount over the face value. The premiums are usually put in the context of the percentage over the face value. For example, say that I purchase a lien for $100 at 5% premium. This means I paid $105 for the lien, $5 above the face value. The lien will accumulate only 83 cents in interest each month, so I will need to hold the lien for at least 6 months to break even. If the buyer redeems the lien before 6 months, I have lost money.

Therefore, in estimating profits from tax liens, the very first step was to estimate the rate of redemption. Information about this is surprisingly scarce on the web. Thankfully, El Paso County publishes redemption statistics.

The statistics are not archived, thus the numbers here may not match up with what is currently on the official website. At the time of September 2014, numbers I got were as follows:

- For tax liens in 2010: 6.7% were still unredeemed at the start of 2014 and 4.87% were still unredeemed in September 2014.

- For tax liens in 2011: 18.47% were still unredeemed at the start of 2014 and 9.9% were still unredeemed in September 2014.

- For tax liens in 2012: 27.1% were still unredeemed at the start of 2014 and 16.23% were still unredeemed in September 2014.

- For tax liens in 2013: 66.10% were still unredeemed at the start of 2014 and 35.5% were still unredeemed in September 2014.

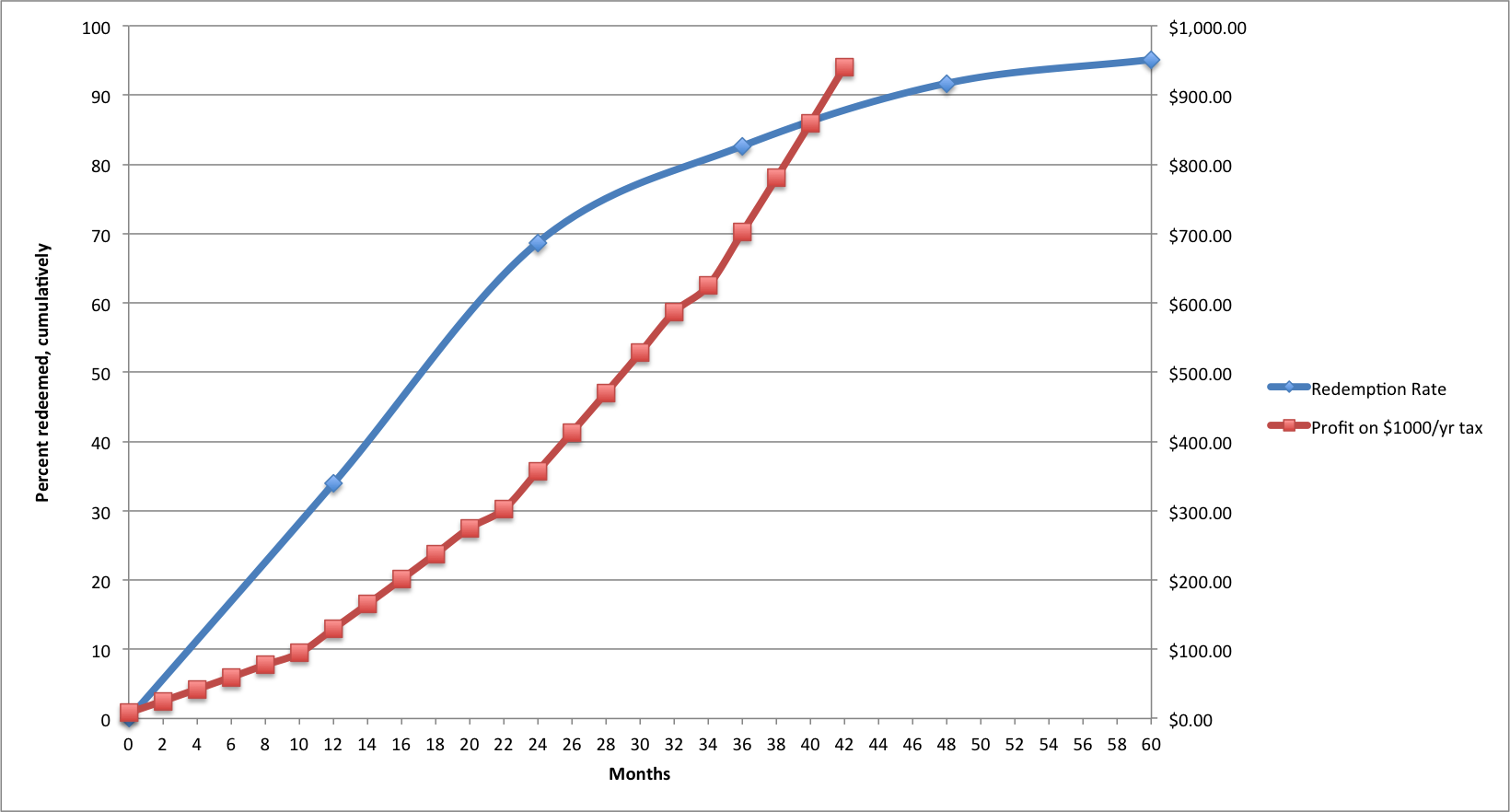

Now, for obvious reasons, it is dangerous to assume that liens issued in El Paso in certain years are representative of Colorado liens or predictive of any future liens. But it’s the best I had to go on. I plotted a graph in Excel:

Tax lien statistics. Red reflects profit on a $1000 investment. Blue reflects the redemption percentage.

So, we can expect 1/3 of liens to be redeemed in the first year, 2/3 in the second year, and 85% by the third year. The 40-month mark is an important milestone, because it is at that point where the lienholder can file to get the property altogether; for that reason, I did not calculate profits beyond that month. The profits assume the holder will subtax the liens, hence the slight jumps at these marks.

In future blog posts, I will explain the Monte Carlo simulator I created with this data, my findings, and my actual experience & returns-to-date.